People often neglect the importance of saving for retirement, as many people fail to address this issue. We’re going to shed some light on this topic and list some of the latest and most fundamental retirement stats.

Nowadays, there’s an increase in the working population over the retirement age limit. This issue has become more pronounced in recent years, as we went through a couple of financial crises, including a major one.

Paying attention to the facts presented below might help thousands of individuals think twice about their incomes, especially when retirement pops its head around the corner.

Without further ado, let’s delve deeper into this topic.

Top 8 Enlightening Retirement Statistics & Facts (Editor’s Choice)

- Over 50% of people who don’t retire at 65 keep working by choice

- People aged 44 to 49 have $113,370 in retirement savings

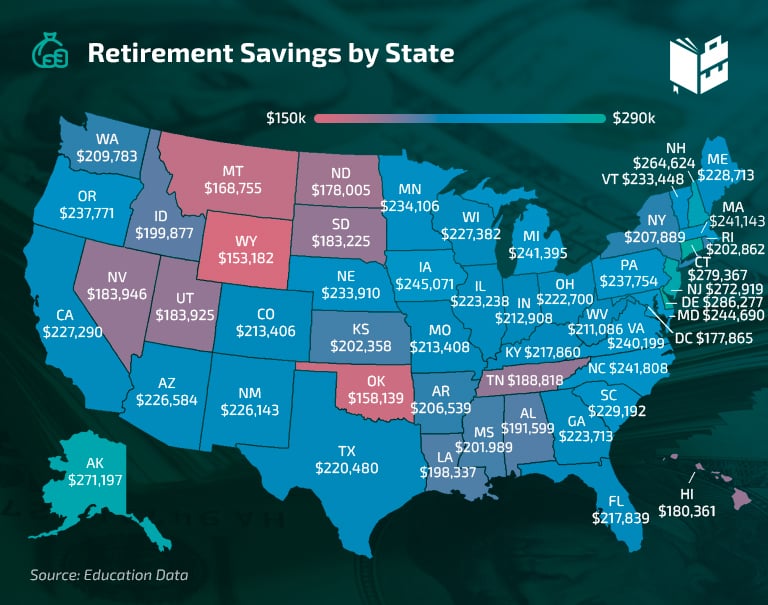

- The retirement savings in Virginia are approximately $240,199

- Women mostly start saving for retirement at the age of 26

- Almost 9 out of 10 retirees who are 65 or older receive social security benefits

- Around 10,000 baby boomers retire daily

- 48% of workers retire early

- An average retired couple needs approximately $295,000 for medical expenses

The Latest Retirement Stats

1. 85% of Americans use a 401(k) plan to save for retirement.

(Source: Northwestern Mutual)

401(k) is, undoubtedly, the most popular retirement saving method in the US. The average account of an American worker in their 40s has $103,500 in it. This popularity stems from the contribution matching what some employers offer.

2. A whopping $11 trillion retirement assets are recorded over various IRAs.

(Source: Axios)

IRAs, or individual retirement accounts, are another popular retirement saving vessel. These accounts offer tax deductions based on the contributions made during the year. According to US retirement statistics, Americans have $11 trillion in traditional, Roth, SEP, and SIMPLE IRAs.

3. The total value of the US federal government retirement funds exceeds $4 trillion.

(Source: Washington Post)

There are a trillion more available to those who are retiring, as these retirement facts stress. However, the US’s pension system is still commonly described as “in an acute state of crisis.” Unfortunately, retirement funds include only 2% of the upper class’s wealth.

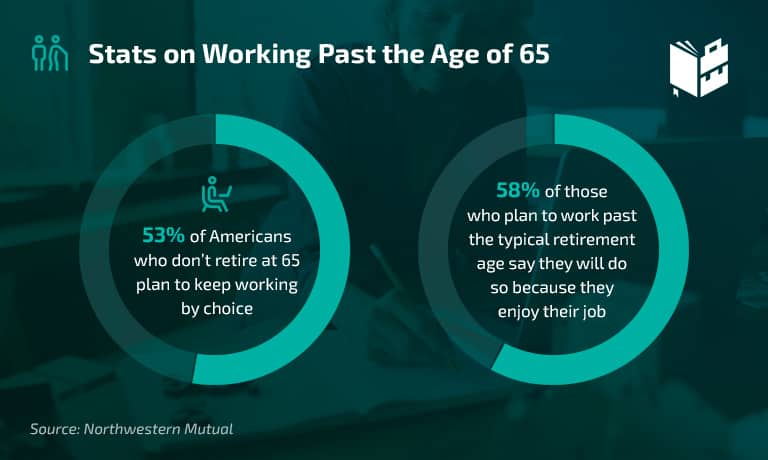

4. 53% of Americans who don’t retire at 65 plan to keep working deliberately.

(Source: Northwestern Mutual)

More than half of American workers who plan to work past the age of 65 will do so by choice. Approximately 58% of those who declared they’ll work after the typical retirement age say they will do so because they enjoy their job.

These fun facts about retirement also show that 39% plan on not retiring to avoid being bored and becoming inactive, while 46% will continue working because they want additional income.

5. Only 26% of Americans have a backup plan if they get an early retirement.

(Source: Debt)

People might retire early unexpectedly, primarily because of health problems, job loss, accidents that could cause disabilities, etc. A good retirement plan includes savings and disability or long-term care insurance.

6. 30% of Americans made early retirement withdrawals during the first stages of the coronavirus pandemic.

(Source: Magnify Money)

According to retirement crisis statistics, the coronavirus outbreak forced 3 in 10 US citizens to withdraw retirement funds early from their accounts. Furthermore, an additional 19% of Americans potentially planned to withdraw in the future.

7. Retirement lasts longer than 13 years for some people.

(Source: Investopedia)

Even if the average time spent in retirement is around 13 years, some people are retired much longer than that. A 65-year-old person has a 50% chance of making it to 84 to 86.5.

Average Retirement Savings Statistics

8. 22% of Americans have less than $5,000 in retirement savings.

(Source: CNBC)

Many retirement reports indicate that more than a fifth of American workers have put under $5,000 in their retirement savings accounts. Approximately 5% of the US workers have saved around $5,000 to $24,999, while only 16% have saved $200,000 or more.

Furthermore, this retirement statistic also shows that 46% of Americans have no idea of the amount they should save for retirement, which is quite worrying.

9. 15% of Americans have no retirement savings.

(Source: Northwestern Mutual)

Less than half of all Americans have no clue about how much they’ve saved, and 15% of US citizens have no savings at all. That includes every worker across the US, even those 20 years old or younger.

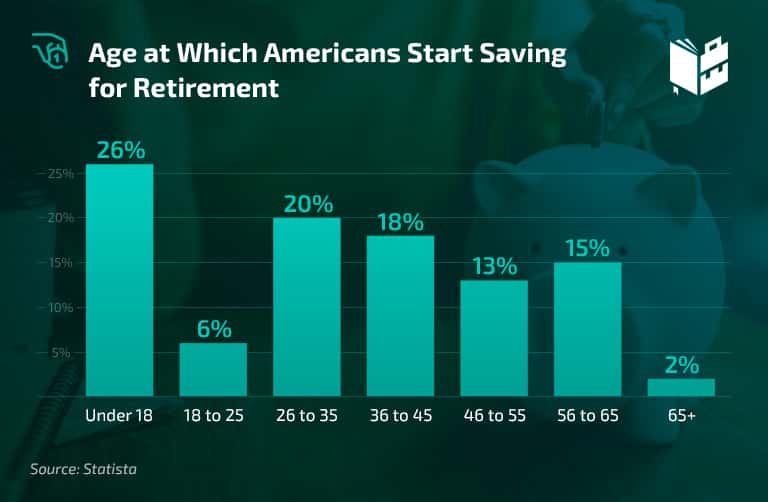

10. 48% of Americans start their retirement savings after the age of 36.

(Source: Statista)

According to these American retirement saving statistics, almost half of the US labor force starts saving for retirement after turning 36. Even though this may not seem like a late game-changing shift, it still puts them at a significant disadvantage compared to those who started saving in their 20s.

11. Millennials have a median total of $23,000 saved for retirement.

(Source: Trans America Center)

The latest recruitment survey of workers in the US indicates that millennials’ median amount of retirement savings is $23,000. Statistics on median retirement savings by age show that millennials save seven times less than the baby boomer generation.

However, it’s good to point out that most millennials keep up with the recommended savings and will have one year’s salary worth in retirement funds by the age of 30.

12. People aged 32 to 37 have around $32,602 saved for retirement.

(Source: The Balance)

American workers in their 30s are not so good at keeping up with the recommended retirement contributions.

Retirement statistics by age point out that they are typically at less than half of the recommended $67,000. Those between the ages of 38 and 43 have an average of $61,933 saved for retirement.

13. People aged 44 to 49 have $113,370 saved for retirement, on average.

(Source: The Balance)

With a median income of $67,000, American workers in their middle to late 40s manage to save over $80,000 on average. Namely, the average amount saved for retirement for this age group sits at $113,370.

Retirement Statistics by State and Age

14. Delaware has the highest average retirement savings ($286,277).

(Source: Financial Samurai)

The tax benefits Delaware offers really shine through. This is the state with the highest average retirement savings in the country.

There’s no state income tax, untaxed Social Security benefits, and no personal property tax. Many more benefits have contributed to this status.

15. The average retirement savings in Alaska are at $271,919.

(Source: Financial Samurai)

When it comes to the retirement facts and statistics by state, Alaska is near the top of the list of US states and is now ranking fourth. Again, low taxes are to thank for this; Alaska has no state and local taxes on retirement income. This applies to both public and private pension income.

16. The retirement savings in Virginia are at around $240,199.

(Source: Smart Asset)

Even though the state is just a thousand dollars short of entering the top 10 US states by average retirement savings list, Virginia is still considered one of the more pensioner-friendly states.

Stats and retirement income figures for this state are aided by no local taxes and the low retirement tax rates (under 1% for pre-tax income of $40,000).

17. The average retirement savings in California are at $227,290.

(Source: Smart Asset)

California ranks 20th on the list of US states by retirement savings. The Golden State also has no local retirement income taxes, while its state tax stays below the 1% mark.

However, the state fully taxes withdrawals from retirement accounts and both the public and private pension incomes. According to these scary retirement statistics, this isn’t a pensioner-friendly state.

18. The average retirement savings in New York are at $207,889.

(Source: Zippia)

NYS retirement savings place the Empire State in the bottom half of the list. The state of New York holds the 34th spot on the list of states by average retirement savings. Retirees pay a reasonable state tax and no local one.

19. The average retirement age in the US is 61.

(Source: Dave Ramsey)

Even if it seems that the best age to retire is around 61, over 50% of workers plan to work past age 65. Apart from that, many people go back to work after retirement. Some of them work part time, while others pursue a different career.

20. The average age when women start saving for retirement is 26.

(Source: Transamerica Center)

Both men and women start saving for retirement in their 20s. Men usually begin saving at the age of 27, while women start a year earlier.

Retirement Income Statistics

21. The median retired household has a yearly income of $56,632.

(Source: New Retirement)

Older American households with a retiree’s head have an average income of $56,632. However, single households have a considerably lower income. For example, single households aged 65 to 69 have a median income of $32,031.

22. Nearly 9 out of 10 retirees aged 65 or older receive social security benefits.

(Source: SSA)

Workforce retirement statistics find that Social Security contributes close to half of the average pensioner’s yearly budget. 65 million Americans received over $1 trillion in 2020.

23. 50% of American households won’t be able to maintain their standard of living in retirement.

(Source: Good Life)

Half of US workers can’t keep the same standard of living once they retire dubecause ofhe lack of financial support.

That doesn’t only mean that they’ll be unable to travel or buy cars and expensive things. Many retiree statistics indicate they could also struggle with affording necessities like food.

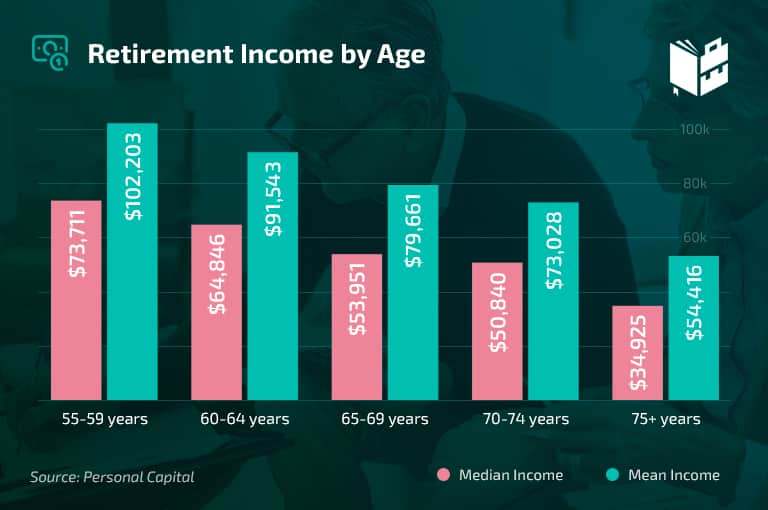

24. Households aged 65 to 69 have a median retirement income of $53,951.

(Source: Personal Capital)

After retiring, those aged 65 to 69 can expect to bring in just a little more than $50,000 per year per household. The mean income for the same age group amounts to $79,661.

25. Households aged 70 to 74 have a median retirement income of $50,840.

(Source: Personal Capital)

Retirement age statistics show that average retirement income drops significantly with age. Those between the ages of 70 and 74 can expect to earn less than those 5-10 years younger. The mean retirement income also drops significantly with age. For this age group, it sits at $73,028.

26. Households aged 75 and over have a median retirement income of $34,925.

(Source: Personal Capital, Good Life)

Elderly households in America are struggling to survive nowadays. With a mean retirement income of $54,416, it’s no wonder that more and more US workers are deciding to keep working in their late 70s. It’s an issue that continues to be a problem across the US and needs to be dealt with promptly.

Baby Boomers Retirement Statistics

27. Around 10,000 baby boomers retire every day.

(Source: Investopedia, USA Today)

There are around 73 million baby boomers in the US. With 10,000 members of this age group retiring every day, we need to address how many of them can enjoy their retirement in comfort.

Retirement also brings new learning opportunities. For example, Udemy offers various knitting and gardening courses (check out our Udemy review to know more).

28. Those aged 56 to 61 have $163,577 saved for retirement on average.

(Source: The Balance)

As this generation approaches the typical retirement age, data on the percentage of income to save for retirement show they usually save 16.35% of the $1,000,000 that experts recommend as the retirement goal.

This is the number one issue on the list of baby boomers retirement problems, and it might be the reason why so many of them plan to continue working after age 65.

29. 17% of baby boomers have saved under $5,000 for retirement.

(Source: CNBC)

A large portion of the generation might not be able to retire, as baby boomer retirement statistics show. This generation is between the ages of 55 and 73. Many have less than $5,000 in retirement savings, which will not get them far if they decide to stop working.

30. 45% of baby boomers have no retirement savings.

(Source: Investopedia)

Around 90% of those who retire are eligible for Social Security benefits. In 1962, that number was 69%. Even with the $1,461 that Social Security brings in every month, a large part of the baby boomer population won’t be able to retire, as they have no funds dedicated to retirement.

31. 68% of baby boomers plan to retire after age 65.

(Source: Northwestern Mutual)

Retirement plan statistics show that 47% of Americans believe they’ll be working after the age of 65 out of necessity. Consequently, 17% of all baby boomers have less than $5,000 in retirement savings and about 20% state they have less than $5,000 in personal savings. Gig economy statistics indicate that baby boomers show interest in freelancing.

32. A third of baby boomers plan on working part-time after the age of 65.

(Source: USA Today)

Around 33% of middle-aged Americans plan to work part-time after reaching their retirement age because their retirement savings prevent them from retiring fully. They also believe that their health, education levels, and experience enable them to do so.

Other Relevant Statistics on Retirement

33. Almost one in two senior women aged 76 or older live alone.

(Source: Yahoo)

One in three people aged 76 or older who don’t live in a nursing home live alone. It seems that women over the age of 75 get more isolated than men. Women are twice as likely to live alone than senior men.

34. The number of military retirees in the US is expected to be around 2.28 million by 2031.

(Source: Statista)

As military retirement statistics point out, the number of military retirees should increase steadily. There are currently around 2.19 million military retirees. People who served in active duty, guard, or reserves for at least 20 years have military retirement pay.

35. Nearly 70% of people who are 50 or older regularly recycle.

(Source: Yahoo)

Older people think green. Namely, around 70% of senior people use energy-efficient bulbs. However, only about 33% buy locally grown food, and approximately 2% lease or own hybrid vehicles.

36. 48% of workers retire before they think they will.

(Source: The Balance)

According to early retirement statistics and other data, nearly half of US citizens retire before they plan to do so. Early retirement can happen to anyone. Therefore, people need to keep that in mind and save more money.

37. An average couple needs around $295,000 for medical expenses in retirement.

(Fidelity)

Healthcare is one of the biggest expenses in retirement. An average couple needs almost $300,000 for medical expenses, excluding long-term care.

Retirees will spend around 18% of that amount on generics and drugs, 39% on appointments and hospital visits, and 43% on other medical expenses.

Retirement Stats – Summary

Retirement savings are one of life’s most crucial aspects that people forget pretty easily. Saving will enable you to find a perfect place to retire, travel, and live with no worries.

Getting into a habit of putting aside a small sum of your income for retirement is best done early in life. Those who start saving in their 20s will have fewer issues when retirement knocks on the front door than those who start saving in their 40s.

We genuinely hope the facts we presented in this article will make you think seriously about saving early for retirement.