Many student loan debt statistics reveal that more and more people are struggling with their payments. Many young people have given up because they can’t afford to get a loan. Most importantly, this trend hasn’t seemed to slow down over the years.

On the contrary, it’s getting worse and affects the country’s entire economy. Experts claim that student loans prevent young Americans from becoming entrepreneurs.

Let’s take a look at the numbers behind these worrying facts.

Key Student Loan Debt Facts & Stats (Editor’s Choice)

- The average medical school debt is $215,900

- 46 million US citizens have student loans

- Almost 7% of students apply for loan forgiveness

- Students from California owe $138 billion

- One-third of those aged 25 to 34 got in debt to get a degree

- LGBTQ borrowers owe around $16,000 more than their peers

- 94% of all student loan debt are FFEL loans

- 3.6% of the student loan debt belongs to Perkins loans

Student Loan Debt Statistics for 2021

The last year was especially difficult for students with loan debts. The unemployment rate among students has increased because of the coronavirus pandemic. In this section, you will find the latest statistics and facts about student loan debt and everything you need to know in 2021.

1. Women owe $929 billion in student loan debt.

(Education Data)

Even in 2021, women still need more time to pay off their debts. Furthermore, parents are more likely to help male children financially. In addition to that, women have a 26% lower income than men.

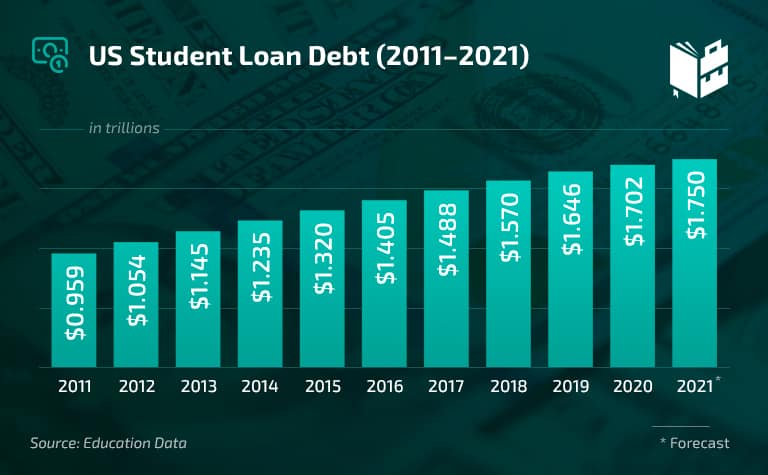

2. The total student loan debt in the US is currently $1.7 trillion.

(Investopedia)

The coronavirus pandemic has had a drastic impact on students and their loan debts, and it seems that the situation won’t improve anytime soon. Students owe almost $1.6 trillion in federal and $132 billion in private student loan debt.

3. The approximate medical school debt is $215,900.

(Education Data)

Loan debts have vastly contributed to the healthcare crisis in the US. A majority of students (76-89%) graduate with educational debt. According to student loan statistics, private medical school graduates owe around $2000 less public medical school graduates.

4. A survey showed that it takes around 18.5 years to repay a student loan debt.

(CNBC)

Student graduates are expected to pay off their debt until they’re 45 years old. However, some students are debt-free before the age of 30. Around 2.6 million loan borrowers are 62 years old or even older.

5. One in eight US citizens has student loans.

(Brookings)

Nowadays, student loans are the second most prominent type of household debt in the US. Luckily, statistics about the average student loan debt after graduation reveal that only 6% of college graduates owe more than $100,000.

6. Generation X carries the highest amount of student loan debt.

(Cardrates)

The borrowers of this age group have an average of $39,584 of debt per person. That’s more than $5,000 more than millennial student loan holders. Baby boomers are right after generation X, with an average of $34,703 in student debt.

General Student Loan Debt Statistics

A majority of students need to borrow money from a private lender or the government to get a college degree. Here, you can find some general statistics and facts about a student loan, borrowers, loan forgiveness, and other topics.

7. About 1% of Americans have student loan forgiveness.

(Student Aid)

As of January 2020, the student loan forgiveness program rejected a shocking 99% of all applications. The program approved loan forgiveness to only 1,565 people who were in debt.

8. The typical monthly rate for student loan payments falls between $200 and $299.

(Federal Reserve)

The monthly average student loan debt per person is between $200 and $299, according to the latest 2020 data issued by this Federal Reserve report. This data shows that the situation has drastically improved over the past few years.

9. 24% of Americans with student loans are behind their payments.

(SPI)

If we go back to the previous years, we’ll note that the rate was lower—the respective share of Americans with late payments was 19% and 20%. Therefore, the average student loan debt is still very high.

10. 52% of the direct federal loan debt is in repayment.

(YouGov)

This category makes up over 50% of the total debt. Only 8% of the student balance is in default, while 40% is “on hold.” The reasons for putting paying the debt back on hold vary and include forbearance, grace period, deferment, or still being in school.

11. 14% of the Class of 2019 parents took $37,200 in federal Parent PLUS loans.

(Student Loan Hero)

In addition to the 69% of that year’s students who took out a loan, 14% of their parents acquired debt. Parents took an average of $37,200 in federal Parent PLUS loans, as college student and other college debt statistics show.

12. The average debt among student loan borrowers in the US is $32,731.

(Valuepenguin)

The loan debt amount depends on the loan and degree type, age, race, and other things. Even if the average loan debt among borrowers in the US is $32,731, borrowers in some states have more debt.

13. 6.7% of students apply for loan forgiveness.

(Education Data)

Even though almost 7% of eligible borrowers apply for loan forgiveness, getting a student loan forgiveness has become almost impossible. Furthermore, student debt data shows that the number of rejected applicants is rising steadily.

14. PSLF servicer approved 2,246 applications for loan discharge.

(Student Aid)

The PSLF servicer approved 2,246 applications and accepted 69% of approved applications for loan discharge. The total amount that was forgiven through this PSLF servicer amounted to a whopping $99 million.

Average Student Loan Debt by Age, State, Race, and Ethnicity

There’s a considerable gap between student loan debt borrowers. Women and people of color usually have higher debt, and they need more time to pay it back. Also, there’s only one state where the average loan debt is under $30,000. Find out more from the following stats and facts.

15. North Dakota is the only state where the average loan debt of students is under $30,000.

(Education Data)

The total loan debt in North Dakota amounts to $2.4 billion. However, student debt statistics reveal that some states have lower total debt, but student borrowers owe more money on average.

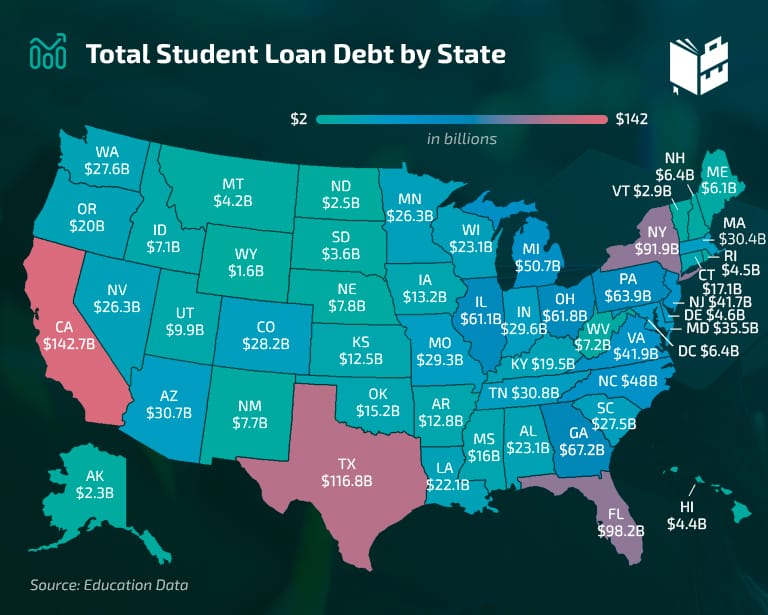

16. Students from California owe $138 billion in total.

(Education Data)

California is one of the states with a higher average loan debt of student borrowers, and it amounts to $36,400. California is in 17th place, while New York is in 7th, and Florida in 4th place.

17. 33% of those aged 25 to 34 got in debt to get a degree.

(Forbes)

The highest number of people who took out a loan to get a graduate degree are between 25 and 34. Facts about student loan debt point out that, although this age group represents the highest percentage of students obtaining a loan, they are not the ones with the most debt.

18. Women hold almost 60% of all student loan debt.

(AAUW)

Women in the US owe approximately $929 billion, which is about two-thirds of the total college debt in the country. That means that women in America are more prone to being in debt after graduation. Also, it takes them longer to pay it off and reach financial stability.

19. 68% of Millennials plan to get in debt loan debt to obtain a Bachelor’s degree.

(New America)

Stats about the percentage of millennials with student loan debt show that about two-thirds of all Millennial students decide to gain a loan to get into college.

Also, 70% of female students and 65% of male students go into debt to get the chance to get a Bachelor’s degree, which increases the stress college students endure.

20. LGBTQ borrowers owe around $16,000 more than their peers.

(Education Data)

Apart from women and people of color, those who identify themselves as members of the LGBTQ population have more debt than their peers.

Apart from that, US student loan debt statistics point out that students who identify as more than one gender have the lowest monthly payment deadline.

21. Black women have the average student loan debt of $37,600.

(Education Data)

Black women have the highest amount of student loan debt among women. Also, while women have $31.300 of average loan debt, Asian female students have the lowest average loan debt.

Other Student Loan Debt Facts and Stats

Colleges and universities aren’t the only ways to educate yourself. Some schools are considerably cheaper. Apart from that, there are all kinds of student loans.

It’s up to young people to choose whether to get in debt or find more affordable schools, courses, or other ways to succeed in life.

22. FFEL loans make up 94% of all student loan debt.

(Department of Education)

The FFEL includes several subtypes of loans – FFEL Plus, FFEL Consolidation, Subsidized Stafford, and Unsubsidized Stafford. Student loan debt data shows that 48.1 million borrowers of FFEL loans in the US owe $145.85 billion.

23. Only 3.6% of the overall student debt belongs to Perkins loans.

(Department of Education)

The Federal Perkins Loan Program helps students with serious financial aid needs. In the second quarter of 2020, approximately 1.9 million borrowers owed $5.6 billion via Perkins loans.

24. Technical college or 2-year vocational school attendees generate student debt of about $10,000.

(College Scholarships)

According to many college student debt statistics, vocational schools and technical colleges are more affordable options than getting a bachelor’s or master’s degree. The average debt for a two-year degree is around $10,000.

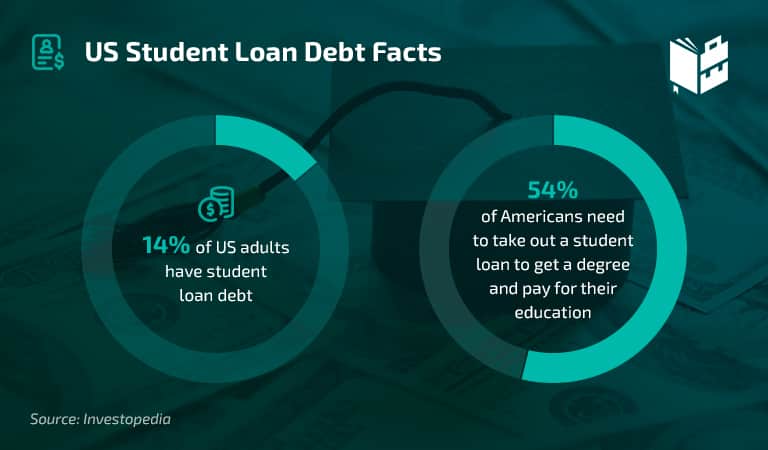

25. 14% of US adults have student loan debts.

(Investopedia)

Nowadays, around 54% of Americans need to take some student loan to get a degree and cover their educational cost, and about one in ten borrowers are behind on their payments.

Student Loan Debt Statistics – Recap

Massive college debt doesn’t just affect the person who’s dealing with it, but it affects their family and the national economy, as well.

As numerous statistics reveal, young Americans must learn from the mistakes of the past. Today, the internet allows us to study from home via one-on-one tutoring sessions or rent out campus books to efficiently deal with the financial aspect of college learning material.

The government also needs to step up its game. Assisting vulnerable individuals and building a better future should be a priority.